RIGHTS AND LIABILITIES OF MORTGAGOR

The Transfer of Property Act, 1882

Dr. Tanmoy Mukherji

Advocate

RIGHTS AND LIABILITIES OF MORTGAGOR [Sections 60 – 66 of the Transfer of Property Act, 1882]-

Tanmoy Mukherji

Advocate

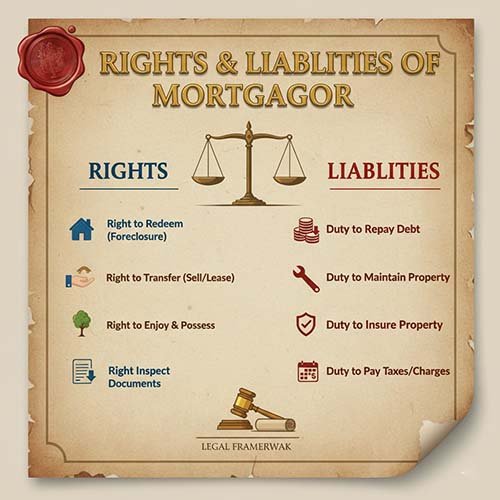

In mortgage, mortgagor does not cease to be the owner of the property mortgaged. The interest in property transferred is limited, not absolute. Therefore, law confers on mortgagor certain rights. Sections 60 to 66 of the Transfer of Property Act, 1882 lay down the provisions relating to the rights and liabilities of the mortgagor. Section 60 deals with the right of mortgagor to redeem which is of great importance and is discussed separately in detail under the head 'Redemption of Mortgage or The Doctrine of Equitable Redemption'. Section 60A (inserted by the Amendment Act of 1929) defines the obligation of a mortgagee to transfer the mortgage debt to a third person named by the mortgagor. Section 60B (inserted by the Amendment Act of 1929) confers on Mortgagor, right to inspect and take copies of the documents of title relating to the mortgaged property. Section 61 confers on mortgagor, right to redeem separately or simultaneously, where two or more mortgages are executed in favor of the same mortgagee. Section 62 confers on usufructuary mortgagor, right to recover possession of the property together with mortgage deed and other documents. Section 63 deals with accession to mortgaged property. Section 63-A (inserted by the Amending Act 20 of 1929) deals with improvement to mortgaged property. Section 64 provides for renewal of mortgaged lease. Section 65 speaks about implied contracts by mortgagor. Section 65A deals with mortgagor's power to lease the mortgaged property. Finally, Section 66 imposes an imperative duty on mortgagor, not to commit acts of waste as to reduce the value of the mortgaged property.

1. Right of Redemption (Section 60)-

The first and most important right of the mortgagor is the right to redeem. It means right to take back the mortgaged property from the mortgagee by repaying the mortgage money within the stipulated period of time. This topic is discussed separately in detail under the head 'Doctrine of Equitable Redemption'.

2. Obligation to transfer to third party instead of retransfer to Mortgagor (Section 60.A)

Section 60.A, as inserted/added by the Amendment Act of 1929 defines the obligation of a mortgagee to transfer the mortgage debt to a third person named by the mortgagor.

It runs as follows-

Where a mortgagor is entitled to redemption, then, on the fulfillment of any conditions on the fulfillment of which he would be entitled to require a transfer, he may require the mortgagee, instead of retransferring the property, to assign the mortgage debt and transfer the mortgaged property to such third person as the mortgagor may direct and the mortgagee shall be bound to assign and transfer accordingly.

-The rights conferred by this section belong to and may be enforced by the mortgagor or by any encumbrancer notwithstanding an intermediate encumbrance; but the requisition of any encumbrance shall prevail over a requisition of the mortgagor and, as between encumbrancers; the requisition of a prior encumbrancer shall prevail over that of a subsequent encumbrancer.

-The provisions of this section do not apply in the case of a mortgagee who is or has been in possession.

-Section 60.A empowers the mortgagor to require the mortgagee to assign the mortgage debt and transfer the mortgaged property to a third person, directed by him. This is possible only on the fulfillment of any condition on the fulfillment of which he would be entitled to require a retransfer.

-The object of this section is to help the mortgagor to pay off the mortgagee by raising a loan from another person on the same security.

3. Right to Inspection and Production of Documents (Section 60.B)-

Section 60B, as inserted by the Amending Act of 1929, confers on mortgagor, right to inspect and take copies of the documents of the title relating to the mortgaged property.

It runs as follows-

-A mortgagor, as long as his right of redemption subsists, shall be entitled at all reasonable times, at this request and at his own cost, and on payment of the mortgagee's costs and expenses in this behalf, to inspect and make copies of abstracts of, or extracts from, documents of title relating to the mortgaged property which are in the custody or power of the mortgagee.

-This section recognises the right of mortgagor to inspection and copies of deeds of title relating to the mortgaged property which are in the custody of the mortgagee. The cases which denied this right of inspection are no longer good law.

4. Right to redeem separately or simultaneously (Section 61)-

Section 61 confers on mortgagor, right to redeem separately or simultaneously, where two or more, mortgages are executed in favor of the same mortgagee.

It runs as follows-

Before the passing of the present Act, the doctrine of consolidation of mortgages was recognized, under which the mortgagor seeking redemption was bound to redeem all subsisting mortgages in favor of the same person in respect of the same property. Amendment Act, 1929, abolished the doctrine of the consolidation of mortgages. But this section abolished consolidation where different properties were mortgaged, and not where the same property was mortgaged under several mortgages. The result was that a mortgagee who had successive mortgages of the same property could consolidate them and compel that all mortgages should be redeemed together. This was inequitable and was altered by the Amendment Act of 1929 which omits all references to property and thereby abolishes consolidation of mortgages whether in respect of the same property or different properties.

Illustrations:

1. A, the owner of farms Z and Y, mortgages Z to B for Rs.1000 and afterwards mortgages Y to B for Rs.1000. A may institute a suit for the redemption of the mortgage of Z alone, B, the mortgagee, cannot compel A to redeem both Z and Y together.

2. A, the owner of farm Z, mortgages Z to B for Rs.5000. Later, A mortgages Z again to B for Rs.3000. When the principal money becomes due, A may redeem either the prior mortgage of Rs.5000 or latter mortgage of Rs.3000 or both.

5. Right of usufructuary Mortgagor to recover possession (Section 62)- Section 62 confers on the usufructuary mortgagor, right to recover possession of the property together with mortgage deed and other documents.

It runs as follows-

In the case of a usufructuary mortgage, the mortgagor has a right to recover possession of the property together with the mortgage deed and all documents relating to the mortgaged property which are in the possession or power of the mortgagee-

(a) Where the mortgagee is authorized to pay himself the mortgage money from the rents and profits of the property – when such money is paid.

(b) Where the mortgagee is authorized to pay himself from such rents and profits or any part thereof a part only of the mortgage money – when the term (if any) prescribed for the payment of the mortgage money has expired and the mortgagor pays or tenders to the mortgagee the mortgage money or the balance thereof or deposits it in Court as hereinafter provided.

Comments-

The section has been amended by the Amendment Act 20 of 1929, and the amendments make the section correspond with the definition of usufructuary mortgage in Section 58(d).

This section would be read along with Section 60 which lays down that a mortgagor who wants to redeem must pay the mortgage money. In case of a usufructuary mortgage, special provision is made in this section as to when the mortgagor can recover possession of the mortgaged property. Under the terms of the section, in cases where the mortgagee is authorized to pay himself out of the rents and profits of the property, the mortgagor can recover possession only when such money is realized. He cannot pay cash and recover possession. If, on the other hand, the mortgage deed provides for the payment only of interest or part of the mortgage money out of the income, a term may be fixed for the payment of the principal or the balance of the mortgage money, as the case may be. In such a case, the mortgagor can recover possession on the expiry of the term and on payment or tender to the mortgagee of the mortgage money or the balance thereof.

6. Accession to mortgaged property (Section 63)-

Section 63 deals with accession to mortgaged property.

It runs as follows-

Where mortgaged property in possession of the mortgagee has, during the continuance of the mortgage, received any accession, the mortgagor, upon redemption, shall, in the absence of a contract to the contrary, be entitled as against the mortgagee to such accession.

7. Accession acquired in virtue of transferred ownership-

Where such accession has been acquired at the expense of the mortgagee, and is capable of separate possession or enjoyment without detriment to the principal property, the mortgagor desiring to take the accession must pay to the mortgagee the expense of acquiring it. If such separate possession or enjoyment is not possible, the accession must be delivered with the property; the mortgagor being liable, in the case of an acquisition necessary to preserve the property from destruction, forfeiture or sale, or made with his assent, to pay the proper cost thereof, as an addition to the principal money, with interest at the same rate as is payable on the principal, or where no such rate is fixed at the rate of nine per cent per annum.

-In the case last mentioned the profits, if any, arising from the accession shall be credited to the mortgagor.

-Where the mortgage is usufructuary and the accession has been acquired at the expense of the mortgagee, the profits, if any, arising from the accession shall, in the absence of a contract to the contrary, be set off against interest, if any, payable on the money so expended.

-Any addition to the mortgaged property is called accession. This accession or addition may be brought either by the nature or by the efforts of the mortgagee. However the 'accession' primarily denotes physical accretions or addition whether brought about by natural or artificial means.

-The general rule is that where mortgaged property in possession of the mortgagee has received any accession, the mortgagor upon redemption is entitled to such accession. This is based on the equitable maxim 'accession credit principle' i.e. the increase follows the principal. It is enunciated in Section 63 of the T.P.Act, which is similar to Section 90 of the Indian Trust Act.

Accession or addition may arise in any one of the following-

i) Natural causes.

ii) Acquired by the mortgagee's own cost.

The natural accession of the mortgaged property ensures a benefit to the mortgagee and his family but at the same time it is subject to the redemption by mortgagor. So it goes to the mortgagor.

The acquired accession can be sub divided into-

a) Accession which are separable; and

b) Accession which are inseparable.

Separable Accessions-

When the accessions are acquired by the mortgagee's own cost which are separable from the security shall go to the mortgagee. But if the mortgagor desires to retain them, the mortgagee can surrender them by receiving the cost.

Inseparable Accessions-

When the accession acquired by the mortgagee's own cost cannot be passed or enjoyed by the mortgagee separately from the security, it must be delivered with the property. However, the mortgagor is bound to pay the compensation only in two cases:

(a) Where it was forfeiture of sale Nannumal vs. Ramachandra, 1931 ALJ 275;

(b) Where it was made with the mortgagor's consent.

-In cases where the mortgagor is bound to pay the compensation, he is liable to pay the interest on such cost. The rate of interest should be same what he pays to the mortgagee. If it is not fixed, he should pay at the rate of nine percent per annum.

7. Improvements to mortgaged property (Section 63-A)-

-This section was introduced by the Amending Act 20 of 1929, bears specifically on the point of improvements. Before that, the Act was silent as to improvements by a mortgagee.

-Section 63-A is special provision dealing with improvements effected by a mortgagee in possession.

Section 63-A runs as follows:

-Where mortgaged property in possession of the mortgagee has, during the continuance of the mortgage, been improved, the mortgagor, upon redemption, shall, in the absence of a contract to the contrary, be entitled to the improvement and the mortgagor shall not, save only in cases provided for in sub section (2), be liable to pay the cost thereof.

- Where any such improvement was effected at the cost of the mortgagee and was necessary to preserve the property from destruction or deterioration or was necessary to prevent the security from becoming insufficient, or was made in compliance with the lawful order of any public servant or public authority, the mortgagor shall, in the absence of a contract to the contrary, be liable to pay the proper cost thereof as an addition to the principal money with interest at the same rate as is payable on the principal, or, where no such rate is fixed, at the rate of nine per cent per annum, and the profits, if any, accruing by reason of the improvement, shall be credited to the mortgagor.

8. Renewal of Mortgaged lease (Section 64)-

Section 64 provides for the renewal of mortgaged lease. The old section referred to a lease 'for a term of years'. The words 'for a term of years' have been omitted by the Amending Act 20 of 1929 as unnecessary.

Section 64 runs as follows-

Where the mortgaged property is a lease, and the mortgagee obtains a renewal of the lease, the mortgagor, upon redemption, shall, in the absence of a contract by him to the contrary, have the benefit of the new lease.

9. Implied contracts by mortgagor (Section 65)-

This section makes provisions of the implied contract by the mortgagor for the benefit of the mortgagee.

It runs as follows-

In the absence of a contract to the contrary, the mortgagor shall be deemed to contract with the mortgagee-

(a) That the interest which the mortgagor professes to transfer to the mortgagee subsists, and that the mortgagor has power to transfer the same;

(b) That the mortgagor will defend, or, if the mortgagee be in possession of the mortgaged property, enable him to defend, the mortgagor's title thereto;

(c) That the mortgagor will, so long as the mortgagee is not in possession of the mortgaged property, pay all public charges accruing due to the property;

(d) And, where the mortgaged property is a lease that the rent payable under the lease, the conditions contained therein, and the contracts binding on the lessee have been paid, performed and observed down to the commencement of the mortgage; and that the mortgagor will, so long as the security exists and the mortgagee is not in possession of the mortgaged property, pay the rent reserved by the lease, or, if the lease be renewed, the renewed lease, perform the conditions contained therein and observe the contracts binding on the lessee, and indemnify the mortgagee against all the claims sustained by reason of the nonpayment of the said rent or the nonperformance or non-observance of the said conditions and contracts;

(e) And, where the mortgage is a second or subsequent encumbrance on the property, that the mortgagor will pay the interest from time to time accruing due on each prior encumbrance as and when it becomes due, and will at the proper time discharge the principal money due on such prior encumbrance.

-The benefit of the contracts mentioned in this section shall be annexed to and shall go with the interest of the mortgagee as such, and may be enforced by every person in whom that interest is for the whole or any part thereof from time to time vested.

10. Mortgagor’s power to lease (Section 65.A)-

This section was added/inserted by Section 30 of the Amendment Act of 1929.

It runs as follows-

(1) Subject to the provisions of sub section (2), a mortgagor, while lawfully in possession of the mortgaged property, shall have power to make leases thereof which shall be binding on the mortgagee.

(2)(a) Every such lease shall be such as would be made in the ordinary course of management of the property concerned and in accordance with any local law, custom or usage.

b) Every such lease shall reserve the best rent that can reasonably be obtained, and no premium shall be paid or promised and no rent shall be payable in advance.

(c) No such lease shall contain a covenant for renewal.

(d) Every such lease shall take effect from a date not later than six months from the date on which it is made.

(e) In the case of a lease of buildings, whether leased with or without the land on which they stand, the duration of the lease shall in no case exceed three years, and the lease shall contain a covenant for payment of the rent and a condition of reentry on the rent not being paid within a time therein specified.

3. The provisions of sub section (1) apply only if and as far as a contrary intention is not expressed in the mortgage deed; and the provisions of sub section (2) may be varied or extended by the mortgage deed and, as so varied and extended, shall, as far as may be, operate in like manner and with all like incidents, effects and consequences, as if such variations or extensions were contained in that sub section.

11. Waste by Mortgagor in possession (Section 66)-

Section 66 imposes an imperative duty on mortgagor not to commit any acts of waste as to reduce the value of the mortgaged property.

It runs as follows-

A mortgagor in possession of the mortgaged property is not liable to the mortgagee for allowing the property to deteriorate; but he must not commit any act which is destructive or permanently injurious thereto, if the security is insufficient or will be rendered insufficient by such act.

Explanation-

A security is insufficient within the meaning of this section unless the value of the mortgaged property exceeds by one third, or, if consisting of buildings, exceeds by one half, the amount for the time being due on the mortgage.

we believe in a holistic approach to legal education building not just lawyers, but socially conscious leaders of tomorrow.