Residential status of an assessee

Dr. Tanmoy Mukherji

Advocate

Residential status of an assessee

Tanmoy Mukherji

Advocate

Residential status:

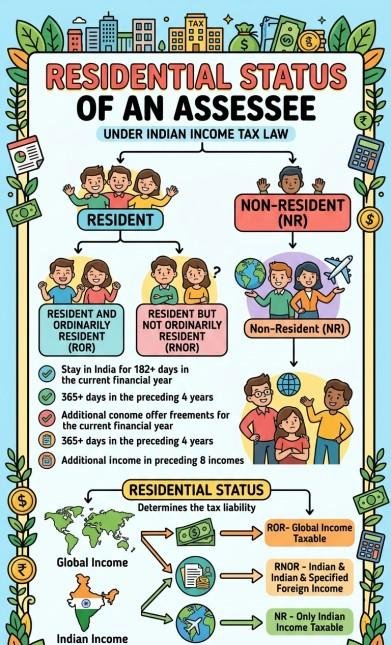

There are two types of taxpayers - resident in India and non-resident in India. Indian income is taxable in India whether the person earning income is resident or non-resident. Conversely, foreign income of a person is taxable in India only if such person is resident in India. Foreign income of a non-resident is not taxable in India.

Criteria for deciding residential status:

i) Different taxable entities-

All taxable entities are divided in the following categories for the purpose of determining residential status:

a) an individual;

b) Hindu undivided family;

c) a firm or an association of persons;

d) a joint stock company; and

e) and every other person.

ii) Different residential status-

The table given below highlights the different residential status of different taxable entities:

|

Category

|

Individual/Hindu undivided family

|

firm, association of persons, joint stock company and every other person

|

|

Category-1

|

Resident in India → Ordinarily resident

→ Not ordinarily resident

|

Resident in India

|

|

Category-2

|

Non-resident in India

|

Non-resident in India

|

iii) Residential status for each previous year-

Residential status of an assessee is to be determined in respect of each previous year as it may vary from previous year to previous year.

iv) Different residential status for different previous year in same assessment year not possible-

If a person is resident in a previous year relevant to an assessment year in respect of any source of income, he shall be deemed to be resident in India in the previous year relevant to the same assessment year in respect of each of his other sources of income [Sec. 6(5)]

v) Different residential status for different assessment years-

An assessee may enjoy different residential status for different assessment years, for instances, an individual who has been regularly assessed as resident and ordinarily resident has to be treated as non-resident in a particular assessment year if he satisfies none of the conditions of section 6(1) in that year.

vi) Resident in India and abroad-

It is not necessary that a person who is resident in India cannot become resident in any other country for the same assessment year. A person may be resident in two or more countries at the same time. It is therefore, not necessary that a person who is resident in India will be non-resident in all other countries for the same assessment year.

How to determine residential status of an individual-

An individual may be -

a) resident and ordinarily resident in India.

b) resident but not ordinarily resident in India or

c) non-resident in India.

a) Resident and ordinarily resident [sec. 6(1), 6(6)(a)]-

To find out whether an individual is resident and ordinarily resident in India one has to proceed as follows.

|

Step-1:

|

First find out whether such individual is resident in India.

|

|

Step-2:

|

If such individual is resident in India, then find out whether he is ordinarily resident in India. However, if such individual is a non-resident in India, then no further investigation is necessary.

|

Basic conditions to test to when an individual is resident in India:

Under sec-6(1) an individual is said to be resident in India in any previous year, if he satisfies at least one of the following Basic Conditions-

|

Basic condition (a) |

He is in India in the previous year for a period of 182 days or more.

|

|

Basic condition (b)

|

He is in India for a period of 60 days or more during the previous year and 365 days or more during 4 years immediately preceding the previous year.

|

Exceptions:

The aforesaid rule of residence is subject to the following exceptions:

i) Exception one (special case-1)-

In special case 1, the period of 60 days referred to in basic condition (b) above has been extended to 182 days by virtue of explanation 1(a) to section 6(a).

However, special case 1 is available in the case of an Indian citizen who leaves India during the previous year for the purpose of employment outside India or an Indian citizen who leaves India during the previous year as a member of the crew of an Indian ship.

ii) Exception-2 (special case-2) -

In special case 2, the period of 60 days referred to in basic condition (b) above has been extended to 182 days by virtue of explanation (b) to Section 6(1). However, special case 2 covers an Indian citizen or a person of Indian origin who comes on a visit to India during the previous year. A person is deemed to be of Indian origin if he or either of his parents or any of his grandparents was born in undivided India. It may be noted that grand-parents include both maternal and paternal grand-parents.

Additional conditions to test as to when a resident individual is Ordinarily resident in India.

Under section 6(6), a resident individual is treated as resident and ordinarily resident in India, if he satisfies the following additional conditions:

|

Condition

|

Description

|

|

Additional condition (i)

|

He has been resident in India at least 2 out of 10 previous years immediately preceding the relevant previous year.

|

|

Additional condition (ii)

|

He has been in India for a period of 730 days or more during 7 years immediately preceding the relevant previous year.

|

b) Resident but not ordinarily resident (sec. 6(1), 6(6), 6(a), 6(b))-

An individual becomes resident but not ordinarily resident in India in any of the following circumstances:

|

Case-(1):

|

If he satisfies at least one of the basic conditions but none of the additional conditions.

|

|

Case-(2):

|

If he satisfies at least one of the basic conditions and one of the two additional conditions.

|

c) Non-resident:

An individual is a non-resident in India if he satisfies none of the basic conditions. In case of non-resident additional conditions are not relevant.

we believe in a holistic approach to legal education building not just lawyers, but socially conscious leaders of tomorrow.