Computation of Direct Tax

Dr. Tanmoy Mukherji

Advocate

Computation of Direct Tax-

Tanmoy Mukherji

Advocate

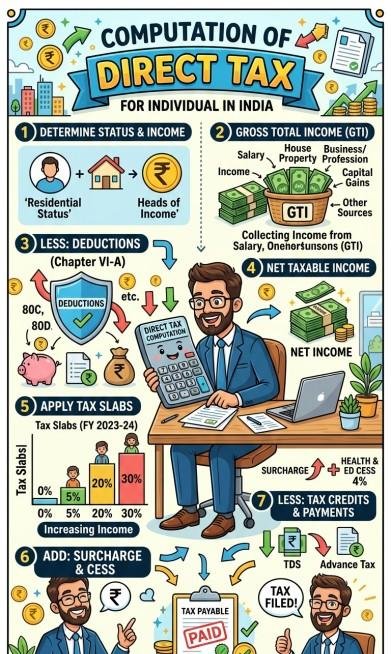

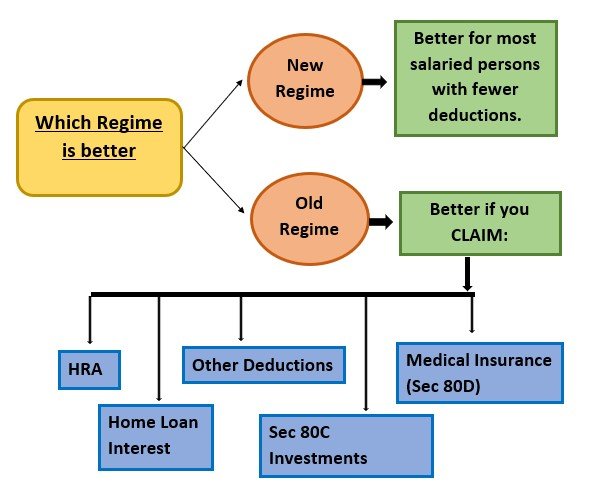

Section 115 BAC provides an alternative and simplified scheme of taxation for tax payers. The scheme offers lower rate of tax with limited exemptions / deductions from income.

The Union Budget 2026-27 has arrived with a clear mandate -

→Simplification through the formal operationalisation and implementation of the Income Tax Act, 2025, effective from 1st April 2026, and

→Discipline through changes in the Securities Transaction Tax (STT) on Future and Options (F&O).

These moves will influence disposable income, savings decisions, and risk appetite for the salaried individuals, traders, and retail investors in India.

Income Tax Slab (FY 2026 - 2027 / AY 2027 - 2028)-

New Tax Regime (Default Regime)-

|

Annual Income |

Tax Rate

|

|

Up to ₹4,00,000 |

Nil

|

|

₹4,00,001 – ₹8,00,000 |

5% |

|

₹8,00,001 – ₹12,00,000 |

10% |

|

₹12,00,001 – ₹16,00,000 |

15%

|

|

₹16,00,001 – ₹20,00,000 |

20%

|

|

₹20,00,001 – ₹24,00,000 |

25% |

|

Above ₹24,00,000 |

30%

|

→Standard Deduction: ₹76,000 for salaried employees.

→Tax Rebate: Available under Section 87A (conditions apply).

→Income up to approximately ₹12 lakh may become effectively tax-free under rebate provisions in many salaried cases.

Old Tax Regime-

|

Annual Income |

Tax Rate

|

|

Up to ₹2,50,000 |

Nil

|

|

₹2,50,001 – ₹5,00,000 |

5%

|

|

₹5,00,001 – ₹10,00,000 |

20% |

|

Above ₹10,00,000 |

30%

|

Senior Citizens (60–80 years)-

|

Annual Income |

Tax Rate

|

|

Up to ₹3,00,000 |

Nil

|

|

₹3,00,001 – ₹5,00,000 |

5% |

|

₹5,00,001 – ₹10,00,000 |

20%

|

|

Above ₹10,00,000 |

30%

|

Super Senior Citizens (80+ years)-

|

Annual Income |

Tax Rate

|

|

Up to ₹5,00,000 |

Nil

|

|

₹5,00,001 – ₹10,00,000 |

20%

|

|

Above ₹10,00,000 |

30%

|

Marginal Relief-

Marginal relief under sec 87A of the Income Tax Act, it ensures that tax payers whose income exceeds ₹ 12 lakhs by a small margin don't pay more tax than their incremental income. Without marginal relief, a small increase in income above ₹ 12 lakhs could lead to a disproportionately higher tax liability.

Working Procedure of Marginal Relief for income slightly above rupees 12 Lakhs-

Marginal Relief ensures that the additional tax payable don't exceed the incremental income over ₹ 12 Lakhs.

This means-

i) If your income exceeds ₹ 12 Lakhs by ₹ 10,000, the maximum additional tax you will pay ₹ 10,000.

ii) Marginal Relief applied only to income up to ₹ 12.75 lakh, after which normal tax calculation apply.

Mr. Y's Tax Calculation-

Gross Taxable Income ₹ 14,00,000. Mr. Y earns Gross taxable salary ₹ 14,00,000.

→Deduction available even under the new regime, taxpayers can utilize specific deduction to lower the taxable income.

→Standard deduction ₹ 75,000 (Under the new tax regime).

→Employer's contribution to NPS [Sec 80 CCD (2)] — ₹ 1,00,000

Total Deduction = ₹ 1,75,000

Tax Liability without Marginal Relief-

Since Mr. Y's taxable income exceeds ₹ 12,00,000, he is not eligible for the rebate under sec 87A. His tax liability is calculated based on the slab rate-

|

Income slab |

Tax Rate |

Amount taxed |

Tax amount |

|

₹ (0-4,00,000) |

0% |

₹ 0 |

₹ 0

|

|

₹ (4-8) lakh |

5% |

₹ 4,00,000 |

₹ 20,000

|

|

₹ (8-12) lakh |

10% |

₹ 4,00,000 |

₹ 40,000

|

|

₹ (12-12.25) lakh |

15% |

₹ 25,000 |

₹ 3,750

|

Total tax ₹ 63,750

→Thus, without Marginal Relief, Mr. Y would owe ₹ 63,750 in taxes (excluding cess 4%).

→Cess will be deducted from total income.

Tax liability with Marginal Relief -

→Marginal Relief ensures that the additional tax payable does not exceed the incremental income above ₹ 12,00,000.

→Incremental Income = ₹ (12,25,000 - 12,00,000) = ₹ 25,000

→Excess tax without relief = ₹ 63,750 (Calculated above)

→Marginal relief applied, tax payable is CAPPED at the incremental income, i.e., ₹ 25,000

→With marginal relief Mr. Y's liability is reduced to ₹ 25,000 + 4% Cess = ₹ (25,000 + 1,000) = ₹ 26,000.

Person claiming Marginal Relief-

Marginal Relief is targeted provision designed for-

→Resident — salaried / Non-salaried tax payers.

→Income range, applicable for ₹ (12,00,000 — 12,75,000).

Not eligible -

→Non resident

→HUF

→Other entities.

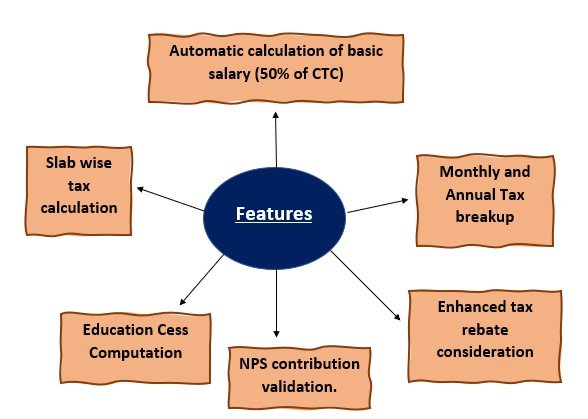

The New Tax Regime Calculator for financial year 2026-27 helps you estimate your income tax liability under the new tax regime. It takes into account your gross income, standard deduction and employer NPS contributions to calculate your tax liability.

As per budget 2026, there were no changes to the tax slabs — they remain the same as the FY (2025-2026).

Tax slabs for FY 2026-27 (No changes from 2025-26)-

|

Income range |

Tax Rate |

Remarks |

|

Up to ₹ 4,00,000 |

Nil |

Tax exempt Income

|

|

₹ 4,00,001 - 8,00,000 |

5% |

₹ 20,000 (max in this slab)

|

|

₹ 8,00,001 - 12,00,000 |

10% |

₹ 40,000 (max in this slab)

|

|

₹ 12,00,001 - 16,00,000 |

15% |

₹ 60,000 (max in this slab)

|

|

₹ 16,00,001 - 20,00,000 |

20% |

₹ 80,000 (max in this slab)

|

|

₹ 20,00,001 - 24,00,000 |

25% |

₹ 1,00,000 (max in this slab)

|

|

Above ₹ 24,00,000 |

30% |

No upper limit.

|

How it works-

The calculator uses the following parameters to compute your tax liability-

→Gross annual income -Your total income for the PY.

→Standard deduction -Fixed deduction of ₹ 75000 for salaried individual

→NPS deduction -Employer contribution to NPS under sec 80 CCD (2)

→Tax rebate -Available for taxable income up to ₹ 12,00,000.

Features-

Importance-

→This calculator is for salaried individuals under the new tax regime.

→All calculations include education cess of 4%

→Enhanced tax rebate ₹ 60,000 is automatically applied for eligible income.

→NPS contribution is capped at 14% of basic salary.

→Standard deduction is automatically considered.

→Tax slab remains unchanged from financial year (2025-26) as per budget 2024.

New Tax Regime Calculator (FY 2025-27)-

Gross annual income (₹)

→ 1000000

Monthly employer NPS calculation (₹)

→5833

Tax calculation summary

Gross income = ₹ 1000000

Basic salary (50% of CTC) = ₹ 500000 (per year)

= ₹ 41667 (per month)

Standard deduction = ₹ 75000

NPS deduction [Sec 80CCD (2)] 14% of basic salary

= ₹ 70000 per year.

Taxable income ₹ 925000

Tax rebate (under sec 87 A) up to 60,000

Total tax ₹ 0

Monthly tax ₹ 0

Take home Yearly ₹ 10,00,000

Take home monthly ₹ 83333

In hand salary (Yearly) ₹ 10,00,000

In hand salary (Monthly) ₹ 83333

In hand = CTC — Employer NPS — Tax excludes PF and other employer deducted components.

Slab wise tax breakdown-

= (4,00,000 - 8,00,000) (5%) = ₹ 20,000

= (8,00,000 - 9,25,000) (10%) = ₹ 12,500

we believe in a holistic approach to legal education building not just lawyers, but socially conscious leaders of tomorrow.