Best Judgement assessment and the remedies available against best judgement assessment-

Dr. Tanmoy Mukherji

Advocate

Best Judgement assessment and the remedies available against best judgement assessment-

Tanmoy Mukherji

Advocate

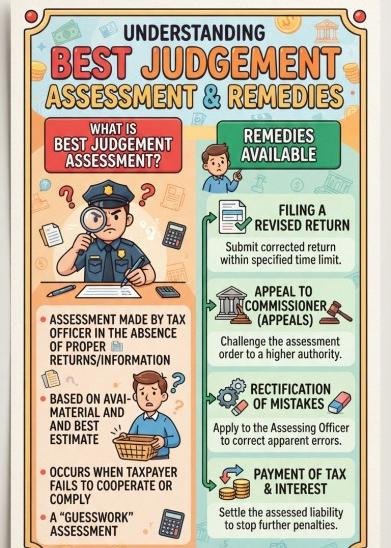

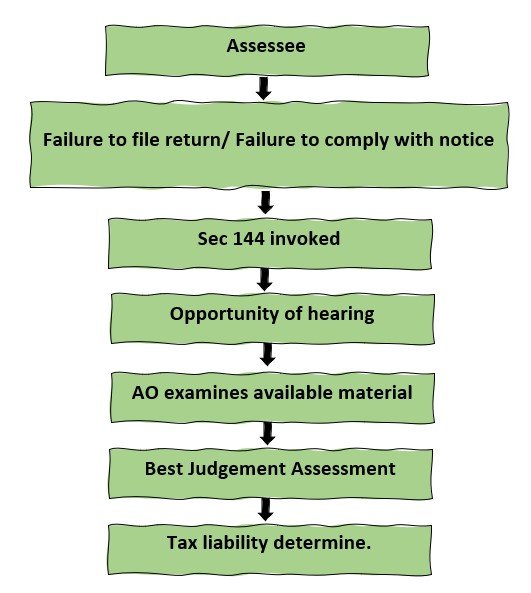

Best Judgement Assessment means and assessment made by the Assessing Officer (AO) based on available information and evidence when the assessee fails to comply with the requirements of the Income tax Act.

Sec 144 empowers the AO to estimate income and determine tax liability according to the best judgement.

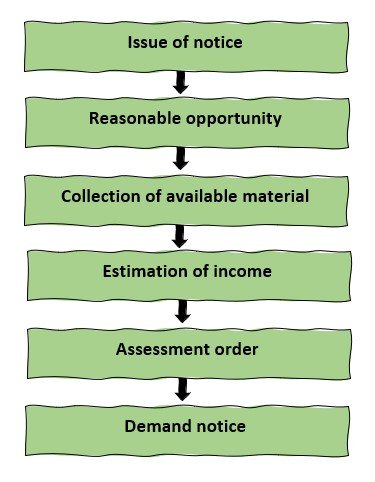

Diagram-

Statutory Provision-

Sec 144 of Income Tax Act, 1961

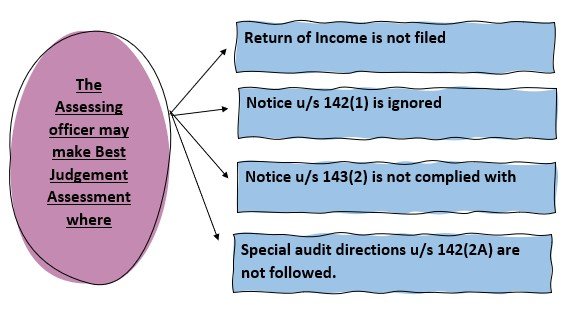

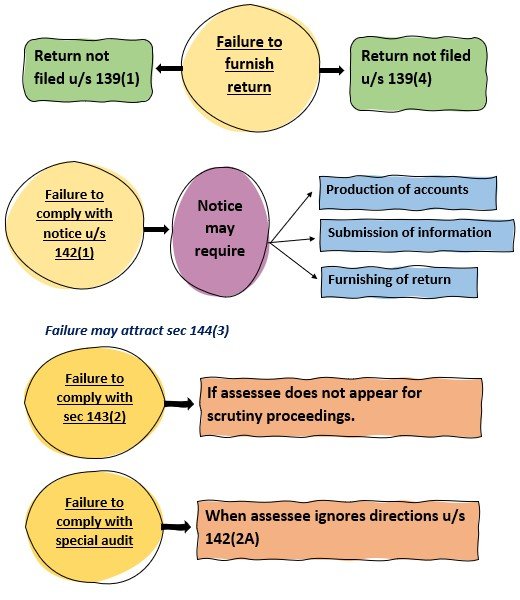

Circumstances for application-

Procedure of Best Judgment Assessment-

Principles governing Best Judgment Assessment-

The Assessor must be-

→Fair

→Rational

→Based on evidence

→Free from arbitrariness

→In confirmation with natural justice

→Honest

Sources used by AO-

The AO may rely upon:

|

Source

|

Example

|

|

Previous returns

|

Past income records

|

|

Bank statements

|

Credits & Transactions

|

|

GST Data

|

Business turnover

|

|

TDS information

|

Form 26 AS

|

|

Market Data

|

Comparable profits

|

|

Third party information

|

Information from customers / suppliers. |

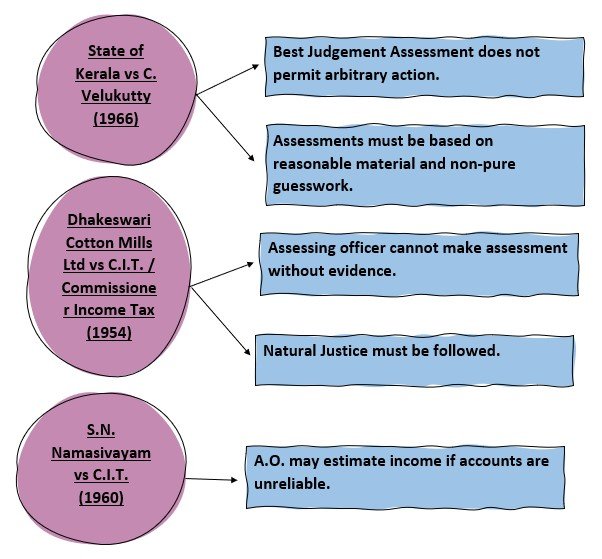

Reference Cases-

Comparative Chart-

|

Particulars

|

Self-Assessment

|

Regular Assessment

|

Best Judgement Assessment

|

|

Provisions

|

Sec 140 A

|

Sec 143(3)

|

Sec 144

|

|

Who calculates tax

|

Assessee

|

A.O.

|

A.O.

|

|

Cooperation required

|

Yes

|

Yes

|

No

|

|

Hearing opportunity

|

Not required

|

Required

|

Required

|

|

Basis

|

Return filed

|

Scrutiny

|

Available materials.

|

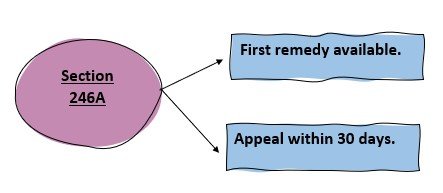

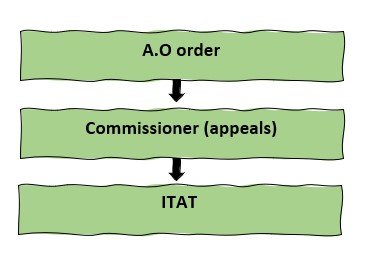

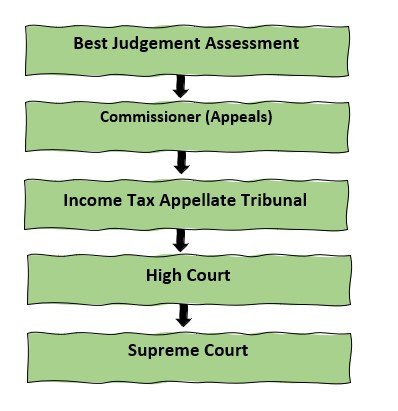

Remedies against Best Judgment Assessment-

Appeal before Commissioner-

Appeal before ITAT (Income Tax Appellate Tribunal)-

If dissatisfied with order of commissioner (Appeals).

Appeal before High Court-

Section 260A- Permitted only on a substantial question of law.

Appeal before Supreme Court-

Final appellate remedy.

Rectification-

Section 154- Where there is an apparent mistake on record.

Example- Calculation errors, Clerical mistakes.

Revision by Commissioner-

Section 264- Commissioner may revise assessment to provide relief to assessee.

Flow Diagram-

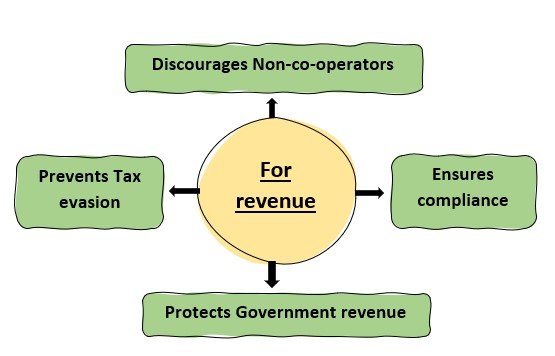

Advantages-

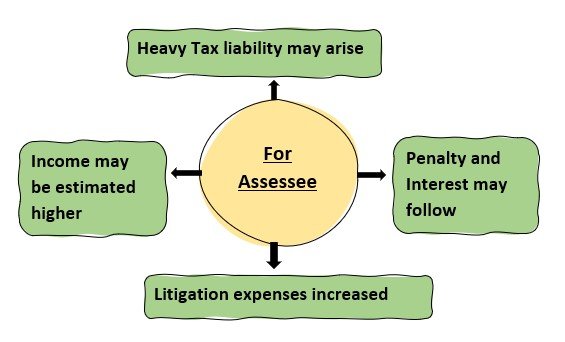

Disadvantages-

we believe in a holistic approach to legal education building not just lawyers, but socially conscious leaders of tomorrow.